The initial fee can range from $10 to $100, while the monthly fee typically runs from $30 to $100 a month, although some companies do charge more. When considering the fees, it’s important to weigh what you’re getting in return.

Full Answer

How do I report derogatory credit to the credit bureaus?

Send a cc of your dispute letter to the creditor, debt collector or bank which sent the derogatory credit information to the credit bureau or bureaus. Also send this via certified mail. The bureau has 30 days to reinvestigate and correct.

What happens if you pay off a derogatory item on credit?

Make sure the accounts are valid before sending payment, especially with debt collection accounts. Paying off a derogatory item doesn’t remove it from your credit report, but your credit report will be updated to show that you’ve paid off the balance.

How long does derogatory information stay on your credit report?

Some types of derogatory information—like a bankruptcy—can remain on your credit report for up to 10 years. Most other derogatory information—late payments and debt collection accounts—will only remain on your credit report for seven years.

How do I remove derogatory marks on my credit report?

You can also remove derogatory marks if they’re inaccurate or unfairly reported. By requesting your free credit report, you can look for mistakes and inaccuracies. For example, check to see if a missed payment was inaccurately reported or if someone else’s account got mixed up with yours.

Can you legally remove things from your credit report?

Bear in mind that correct information cannot be removed from your credit report. So, if your score is being dragged down by accurate negative information, you'll need to repair your credit over time by ensuring you make payments on time and decrease your overall amount of debt.

Can you pay someone to clean up your credit report?

While it may seem like a good idea to pay someone to fix your credit reports, there is nothing a credit repair company can do for you that you can't do yourself for free.

How much does it cost to get something off your credit report?

By law, a credit reporting company can charge no more than $13.50 for a credit report. You are also eligible for reports from specialty consumer reporting companies.

How do I remove derogatory marks from my credit report?

How To Remove Derogatory Items From Your Credit Report | Removing Things from My Credit ReportCheck For Inaccuracies. ... Submit A Dispute To The Credit Bureau. ... Send A Pay For Delete Offer To Your Creditor | How To Remove Derogatory Items From Your Credit Report. ... Make A Goodwill Request For Deletion.More items...•

How many points will my credit score go up when a derogatory is removed?

How much your credit score will increase after a collection is deleted from your credit report varies depending on how old the collection is, the scoring model used, and the overall state of your credit. Depending on these factors, your score could increase by 100+ points or much less.

Can you have a 700 credit score with collections?

Yes, it is possible to have a credit score of at least 700 with a collections remark on your credit report, however it is not a common situation. It depends on several contributing factors such as: differences in the scoring models being used.

How do you ask for goodwill deletion?

If your misstep happened because of unfortunate circumstances like a personal emergency or a technical error, try writing a goodwill letter to ask the creditor to consider removing it. The creditor or collection agency may ask the credit bureaus to remove the negative mark.

How much does it cost to clear credit history?

Credit repair doesn't cost anything if you handle the process yourself. If you hire a credit repair company to assist you, you'll typically pay fees of $19 to $149 per month. There is nothing a credit repair company can do for you that you can't do for yourself.

How do I get a charge-off removed?

Removing Or Disputing A Charge-OffDetermine if the charge-off is accurate. ... Communicate with the creditor. ... Establish a payment plan or settlement. ... Request a Pay-for-Delete arrangement. ... Negotiate re-aging the account. ... Wait it out.

Does removing derogatory marks improve credit?

Removing a derogatory mark from your credit report helps repair your credit. You'll also want to improve your credit by doing things like lowering your credit utilization rate, upping the average age of your credit and making timely payments.

Can a derogatory mark be removed?

If the derogatory mark is in error, you can file a dispute with the credit bureaus to get negative information removed from your credit reports. You can see all three of your credit reports for free on a weekly basis through the end of 2022.

Should I pay off derogatory accounts?

It can be beneficial to pay off derogatory credit items that remain on your credit report. Your credit score may not go up right away after paying off a negative item. However, most lenders won't approve a mortgage application if you have unpaid derogatory items on your credit report.

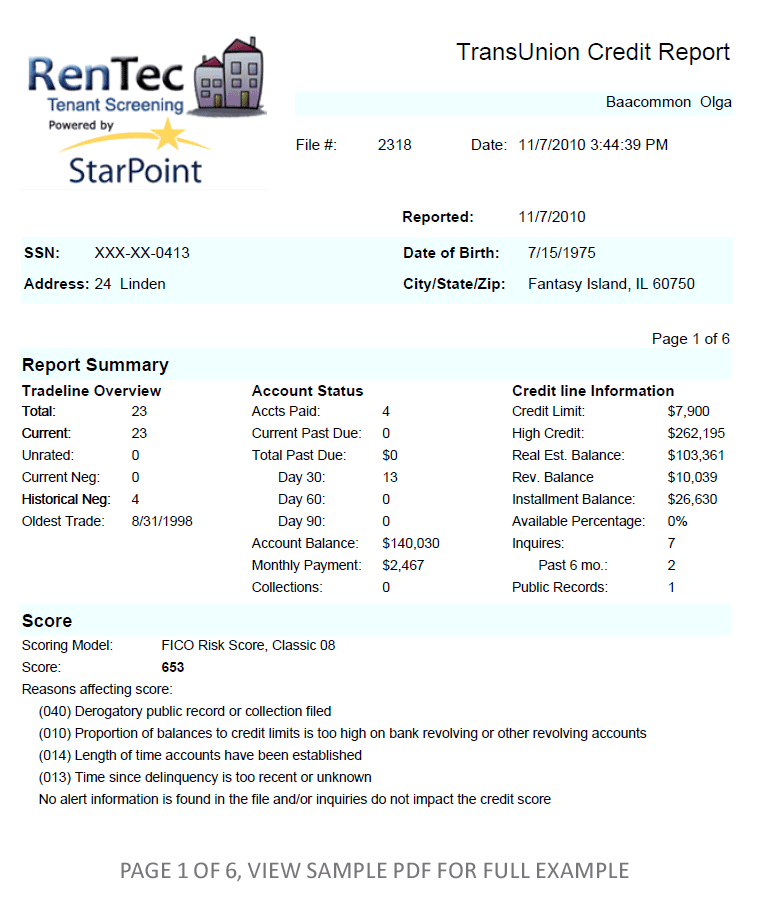

What Are Derogatory Marks On Credit Reports?

Derogatory marks on a credit report are items that reflect negative information about things that were either neglected to be paid on time or not paid at all. This information can include the following:

Strategies for Successfully Disputing Your Credit Report

Derogatory items are easy to get on a report but harder to take off. However, it is possible to get these taken off a credit report. The following are the steps in which you can try on your own to remove derogatory marks:

Solve Derogatory Credit Report Marks With the Help of DoNotPay

DoNotPay helps fix credit report errors in a fast, easy, and successful way! If you want to clean up your credit report but don't know where to start, DoNotPay has you covered in 3 easy steps:

Other Credit Areas That DoNotPay Can Assist In

DoNotPay is the perfect solution for correcting derogatory marks on your credit report and more. Try DoNotPay for yourself and see the difference it can make! To learn more about other areas DoNotPay can help you with on your credit report, check out the following:

What happens if you get derogatory credit?

Having derogatory credit doesn’t automatically mean your applications will be denied, but you’ll have a harder time getting approved with these items on your credit report. If you’re approved with derogatory credit, you may pay higher interest rates, be required to make a down payment or security deposit, or both.

How long does derogatory credit stay on your credit report?

Derogatory credit can follow you around for a long time. Some types of derogatory information—like a bankruptcy—can remain on your credit report for up to 10 years. Most other derogatory information—late payments and debt collection accounts—will only remain on your credit report for seven years.

How do derogatory items affect credit?

Different derogatory items affect your credit score in different ways—some items are given more importance than others. For example, a single late payment will hurt your credit score, but not as much as bankruptcy, which impacts your credit score almost more than anything else. 2 Multiple derogatory items will also cause your credit score ...

What are derogatory items on credit report?

These are the types of derogatory credit items that can appear on your credit report: 1 Late payments, resulting from credit card and loan payments that are more than 30 days late 2 Charge-offs, resulting from debts that have fallen more than 180 days past due and have been written off as uncollectible 3 Debt collections, resulting from debts that have been sold or assigned to a third-party debt collector 4 Foreclosure, resulting from delinquent mortgage payments 5 Repossession, resulting from delinquent auto loan payments 6 Debt settlement, resulting from an agreement between you and a creditor to reduce the outstanding balance and cancel the remainder 7 Bankruptcy, resulting from the legal process of having your debts discharged in court

What is a derogatory credit item?

A derogatory credit item is a result of having negative information on your credit report. Negative items like previous delinquency, high balances, or other items show you’re a potential risk if you borrow more money. This negative information is added to your credit report by the creditors you have accounts with or through public records you have ...

What is a late payment?

Late payments, resulting from credit card and loan payments that are more than 30 days late. Charge-offs, resulting from debts that have fallen more than 180 days past due and have been written off as uncollectible. Debt collections, resulting from debts that have been sold or assigned to a third-party debt collector.

What is debt settlement?

Debt settlement, resulting from an agreement between you and a creditor to reduce the outstanding balance and cancel the remainder. Bankruptcy, resulting from the legal process of having your debts discharged in court. Warning.

How long does it take to remove derogatory items from credit report?

How To Remove Derogatory Items From Credit Report Before 7 Years. You can remove derogatory items from your credit report before seven (7) years. You can use Goodwill letters, negotiate deletions for payment, or send disputes. Each method will work some of the time.

What should a pay for deletion letter include?

A pay-for-delete letter to creditors should include the amount owed, payment conditions, how quickly they should delete the item, and when your offer expires. Then, make sure you get a written letter of acceptance for your offer.

What is credit glory?

Credit Glory is a credit repair company that helps everyday Americans remove inaccurate, incomplete, unverifiable, unauthorized, or fraudulent negative items from their credit report. Their primary goal is empowering consumers with the opportunity and knowledge to reach their financial dreams in 2020 and beyond.

How long do negative items stay on credit?

Negative items can stay on your credit report for up to 7 years. These items include collections, derogatory remarks, and negative items.

How long does a closed account show on your credit report?

Closed accounts in good standing will show on your credit report for 10 years. On the other hand, deragotory accounts are on your report for 7 years.

How to remove negatives before 7 years?

Below are the best methods to remove negative items before 7 years: Dispute negatives with TransUnion, Equifax, and Experian (the "Bureaus") Dispute negatives directly with the original creditors (the "OCs") Send a short Goodill letter to each creditor . Negotiate a "Pay For Delete" to remove the negative item.

How long do you have to remove negatives from Goodwill?

You can use Goodwill letters, negotiate deletions for payment, or send disputes. Each method will work some of the time. If you stay focused and consistent, you can remove your negatives before seven years. Below are the best methods to remove negative items before 7 years:

How to Remove Derogatory Entries From Your Credit Report

Derogatory entries on your credit report, such as 30-day late payments, 60-day late payments, collections, and more, can seriously damage your credit score. Is there a way to get derogatory items removed from your credit report so that your score can bounce back? Let’s find out.

What Are Derogatory Entries on Your Credit Reports?

The term derogatory simply means negative, so derogatory items on your credit report are any items that reflect negatively on your credit. In other words, they indicate that you have failed to make timely payments on your debt.

The Good News: You Can Dispute Inaccurate Derogatory Information on Your Credit Reports

As a consumer, you have the right to have your credit reports be accurate, as dictated by the Fair Credit Reporting Act (FCRA).

The Bad News: You Do Not Have the Right to Have Accurate Negative Information Removed From Your Credit Reports

According to the FCRA, accurate and verifiable negative information can remain on your credit reports for up to seven years.

How to Dispute Derogatory Entries on Your Credit Reports

It is free to dispute inaccurate information on your credit reports, and you can do this process yourself. Another option is to hire a reputable credit repair company to do this work on your behalf.

Working With a Credit Repair Company to Remove Derogatory Information

Although the consumer credit dispute process is free to use, some consumers may choose to work with a credit repair company to accomplish their goals.

How Do You Know if You Need to Dispute Incorrect Information on Your Credit Reports?

To find out if there are errors on your credit reports, you need to get copies of your own reports.

How Long Can Derogatory Marks Impact My Credit Scores

Derogatory marks can remain on your credit for up to seven to 10 years or more, depending on how serious. However, your scores can start improving before that if you take steps to improve your credit health. It can start with making at least the minimum payment on time and keeping your balances low.

Need Help Repairing Your Credit

If youâre struggling with your student loans and have credit issues, I have years of experience helping people just like you. There are plenty of options to get you back on your feet.

Items That Can Cause Derogatory Credit

What is considered derogatory credit? Delinquent credit accounts that are 60 to 90 days past due are considered derogatory credit. Lenders view these delinquent or unpaid accounts as signs that you may not be able to pay them back.

Late And Missed Payments

A payment history riddled with late payments and missed payments is often bad for your credit. While payments that are only a few days late might not show up on your credit report, it will certainly appear if the period advances to 30, 60, or 90 days.

Get A Free Consultation

Most firms offer a free consultation before you sign up to use their services. That call gives you a chance to review your credit history and hear their plan to fix your credit. Its a low-pressure way to get more information about how they can help you.

Limited Access To Credit

In addition to hurting your credit scores, derogatory marks limit your access to credit. Even if your credit scores begin to rebound a few years after the item was filed, potential lenders and credit card companies still see it listed on your credit reports.

Fixing A Derogatory Credit On Your Report

A derogatory credit item is a result of having negative information on your credit report. Negative items like previous delinquency, high balances, or other items show youre a potential risk if you borrow more money.

Credit Assistance Network

It doesn't matter if you are ready to sign up or just need some good advice, don't be shy; we are here to help.

2. Strategies to Remove Negative Credit Report Entries

Submit a Dispute to the Credit Bureau · Dispute With the Business That Reported to the Credit Bureau · Send a Pay for Delete Offer to Your Creditor · Make a What Does Your Credit Report · Credit bureaus · How to Boost Your Credit Score (4) …

3. 4 Ways To Get a Derogatory Mark Off Your Credit Report

Dec 14, 2020 — 4) Write A Goodwill Letter If you did miss a payment but later made the transaction, you can ask your creditor to remove that derogatory mark (7) …

4. Can You Pay to Remove a Bad Credit Report? – Investopedia

Pay for delete is an agreement with a creditor to pay all or part of an outstanding balance in exchange for that creditor removing derogatory information from (9) …

7. How to Get a Derogatory Report Removed With Payment

Creditors are not required to remove derogatory accounts from your credit report if the information is accurate. However, some creditors may be willing to (21) …

10. How long information stays on your credit report – Canada.ca

Jun 7, 2021 — Typically, both Equifax and TransUnion remove a bankruptcy from your credit report 6 years after the date you’re discharged. TransUnion removes (29) …

What to do if you have a derogatory credit report?

If you have a valid derogatory on your credit report, obviously you need to make arrangements to pay it and bring it current. The following steps are intended for those times when you have false or inaccurate information on your credit report. Under federal and state law, credit bureaus and creditors are obligated to remove false ...

How to dispute a derogatory letter?

Keep the letter factual and professional in tone. Send the dispute letter via certified mail to the credit bureau or bureaus which are reporting the false information. Definitely do not do a dispute by phone.

How long does it take for a loan bureau to reinvestigate?

Also send this via certified mail. The bureau has 30 days to reinvestigate and correct. If you are in a hurry because of, say, a pending loan application, the bureaus have an expedited procedure which you can learn about by contacting them. The bureau or bureaus will notify you of the results of their reinvestigation.

Do credit bureaus have to remove inaccurate information?

Under federal and state law, credit bureaus and creditors are obligated to remove false or inaccurate information on your credit report upon receiving notification.

How long does a creditor have to report a charge off?

Accounts sent to collection (within the creditor company or to a collection agency), accounts charged off, or any other similar action may be reported from the date of the last activity on the account for up to seven years plus 180 days after the delinquency that led to the collection activity or charge-off.

What to do if a debt collector doesn't have the authority to act for the original creditor?

If the debt collector doesn't have the authority to act for the original creditor to delete the account information on the original debt, you might need to contact the creditor and the debt collector separately.

What happens if a collection agency agrees to settle for less than you owe?

If the collection agency agrees to settle for less than you owe, be sure it also agrees to report the debt it holds as "satisfied in full" to the credit bureaus. Get written confirmation from the creditor and the collector. The debt collector's confirmation should say that it will acknowledge the debt as paid in full when you pay the agreed amount.

What are the tax consequences of settling debt?

Potential Tax Consequences of Settling Debt. The IRS generally considers canceled debt of $600 or more as taxable, and settling debts for less than what's owed can increase your tax liability depending on your tax bracket and the canceled amount. Consult a tax professional for more information. If the creditor, or the debt collector if it has ...

How often does a debt appear on your credit report?

How Delinquent Debts Are Reported on Your Credit Reports. After your debt has been transferred or sold to a debt collector, it will probably appear twice in your credit history. According to the credit reporting agency Experian, this is how it works: The debt starts as a current, never late account.

What credit bureaus do you use to get your credit report?

Here's how: The three major credit reporting bureaus— Experian, Equifax, and TransUnion —produce credit reports. Ask the collector to tell the bureaus to remove any negative information about the debt from your credit files. The collector might not agree, it might have to get the creditor's approval first, or you might have to pay a bit more on ...

What happens if you sell a collection account to another collection agency?

If the debt is sold again to another collection agency, the status of the first collection account is changed to show that it was sold or transferred. Once again, the final status shows that the first collection account is no longer active, but that status continues to appear as part of the account's history.

Popular Posts:

- 1. who was the lawyer who defended the british soliders in the bosto

- 2. how to start as a federal lawyer

- 3. what is the most expensive lawyer

- 4. how to write letter to lawyer

- 5. how do i become an immigration lawyer in florida

- 6. what personal information does my lawyer need to draw up a will

- 7. what to do if you feel like your lawyer over charged you in oklahoma

- 8. what did rodney dangerfield call his lawyer

- 9. how to keep from lawyer intimidation

- 10. how much does it cost a lawyer to make will