Full Answer

What to do if you have a tax lien on your property?

Thus, if you are experiencing problems with a tax lien, then it may be in your best interest to consult a local tax lawyer for further legal advice.

Why hire a tax lawyer for a tax lien?

Taxation lawyers are already familiar with the tax lien process and forms of acceptable options. Thus, they may be able to provide expert insight and options that are better suited to a particular debtor’s needs.

What is a federal tax lien?

Understanding a Federal Tax Lien A federal tax lien is the government’s legal claim against your property when you neglect or fail to pay a tax debt. The lien protects the government’s interest in all your property, including real estate, personal property and financial assets. A federal tax lien exists after:

Who is a qualifying taxpayer for a tax lien withdrawal?

You are a qualifying taxpayer (i.e. individuals, businesses with income tax liability only, and out of business entities with any type of tax debt) You owe $25,000 or less (If you owe more than $25,000, you may pay down the balance to $25,000 prior to requesting withdrawal of the Notice of Federal Tax Lien)

What happens when IRS puts lien on your house?

A lien secures the government's interest in your property when you don't pay your tax debt. A levy actually takes the property to pay the tax debt. If you don't pay or make arrangements to settle your tax debt, the IRS can levy, seize and sell any type of real or personal property that you own or have an interest in.

How do I negotiate an IRS lien?

Apply With the New Form 656 An offer in compromise allows you to settle your tax debt for less than the full amount you owe. It may be a legitimate option if you can't pay your full tax liability or doing so creates a financial hardship. We consider your unique set of facts and circumstances: Ability to pay.

What is IRS Fresh Start Program?

The Fresh Start Initiative Program provides tax relief to select taxpayers who owe money to the IRS. It is a response by the Federal Government to the predatory practices of the IRS, who use compound interest and financial penalties to punish taxpayers with outstanding tax debt.

Can you buy a house if the IRS has a lien on you?

In a Nutshell Yes, you might be able to get a home loan even if you owe taxes. Owing taxes or having a tax lien does make it harder and more complicated to get a mortgage. You can improve your chances of mortgage approval by actively working to resolve your tax debt even if you can't pay it all off immediately.

How much will the IRS usually settle for?

Each year, the Internal Revenue Service (IRS) approves countless Offers in Compromise with taxpayers regarding their past-due tax payments. Basically, the IRS decreases the tax obligation debt owed by a taxpayer in exchange for a lump-sum settlement. The average Offer in Compromise the IRS approved in 2020 was $16,176.

Can I refinance my mortgage with an IRS tax lien?

If you're trying to refinance your mortgage and have a federal tax lien, you can request that the federal lien be made secondary to your mortgage lender's lien to allow for the transaction to happen.

Does the IRS have an amnesty program?

The most popular and advantageous of the IRS amnesty programs is the IRS Streamlined Procedures. Under this program, a late filer can come clean with the IRS with potentially no penalties by filing tax returns, with all required information returns, for the prior 3 years, and any delinquent FBARs for the prior 6 years.

What is the IRS Hardship Program?

The federal tax relief hardship program is for taxpayers who are unable to pay their back taxes. In other words, taxpayers in need can apply for the IRS' Currently Not Collectable status. You can qualify for the IRS hardship program if you can't pay taxes after paying for basic living expenses.

Does IRS forgive debt after 10 years?

In general, the Internal Revenue Service (IRS) has 10 years to collect unpaid tax debt. After that, the debt is wiped clean from its books and the IRS writes it off. This is called the 10 Year Statute of Limitations.

How long does an IRS lien last?

10 yearsIf you have failed to pay your tax debt after receiving a Notice and Demand for Payment from the IRS and are now facing a federal tax lien, you may be wondering when the lien will expire. At a minimum, IRS tax liens last for 10 years.

How do I get a Judgement lien removed from my house?

Here are some ways to remove a lien from your property.Paying Off the Debt. If you pay off the underlying debt, the creditor will agree to release the lien. ... Negotiating a Partial Payoff. ... Asking the Court to Remove the Judgment Lien. ... Wait for the Statute of Limitations to Expire. ... Filing for Bankruptcy.

Can the IRS seize jointly owned property?

Jointly Owned Assets The IRS can legally seize property owned jointly by a tax debtor and a person who doesn't owe anything. But the nondebtor must be compensated by the IRS, meaning that the co-owner must be paid out of the proceeds of any sale.

How to remove a tax lien?

The safest and best way to ensure that a federal tax lien is completely removed is by paying off the tax debt amount in full. If payment is not possible, then the debtor can request to do one of the following: 1 Set-up an installment payment plan agreement; 2 Complete the application for an online payment agreement; 3 Contact the IRS and ask if they would be willing to compromise by reducing the amount of debt owed; or 4 Check to see if the IRS placed a notice on the debtor’s account that says they are currently unable to pay and that there is a temporary delay on collection.

How to get a federal tax lien removed?

The safest and best way to ensure that a federal tax lien is completely removed is by paying off the tax debt amount in full. If payment is not possible, then the debtor can request to do one of the following: Set-up an installment payment plan agreement; Complete the application for an online payment agreement;

What happens if a debtor declares bankruptcy?

Thus, if the IRS or a state government agency issues a tax lien against a debtor’s property and the debtor declares bankruptcy, then the agency will be required to remove the tax lien on the property. Once a debtor completes the bankruptcy process, however, a government agency may be able to impose a new lien on the debtor’s property.

What happens if a tax lien is already attached to the assets?

Finally, if a tax lien is already attached to the assets and the individual or entity has continued to ignore a government agency’s demand for payment of taxes, then the agency may seize the items contained in the lien documents by using a legal procedure known as a “tax levy”.

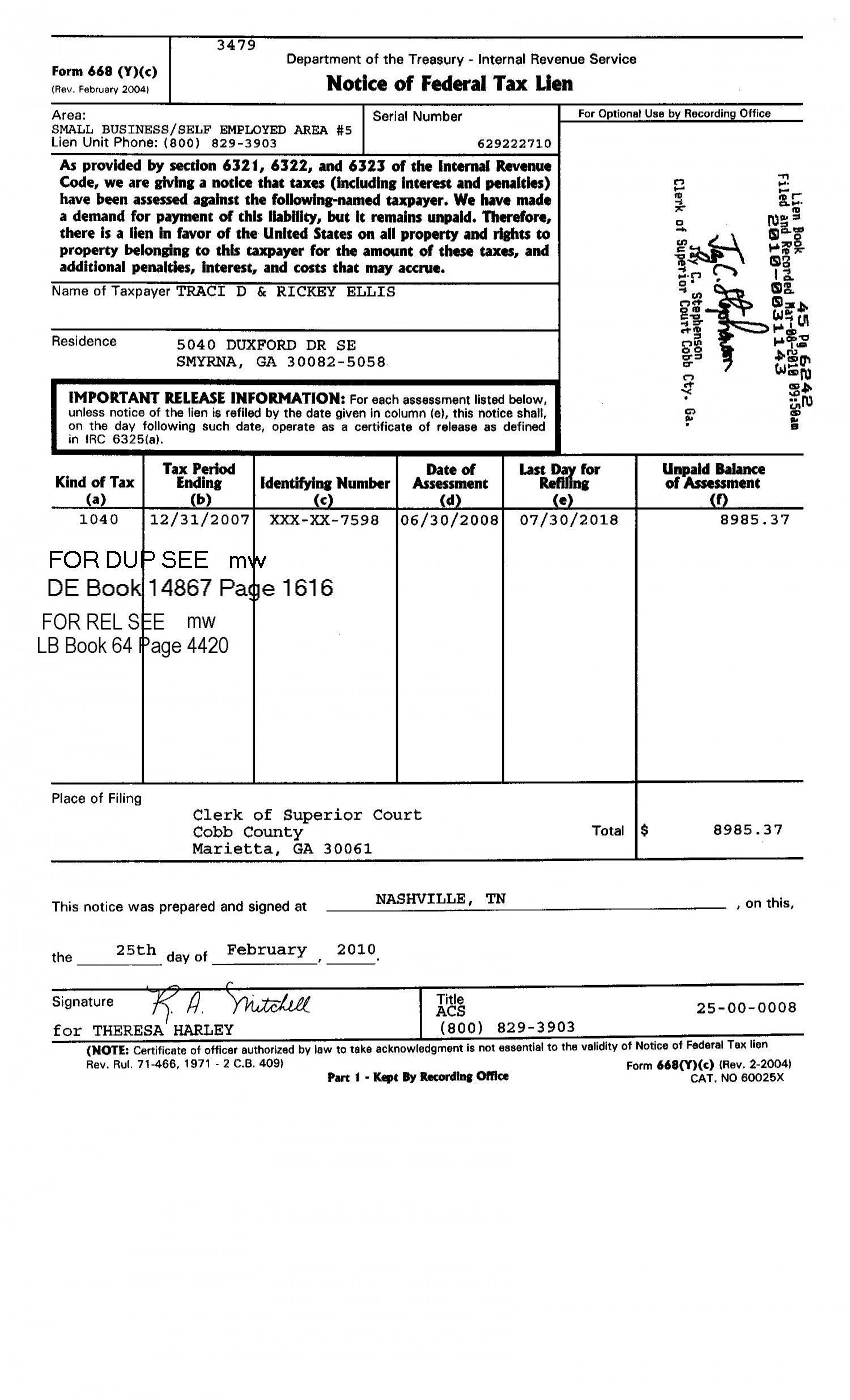

What is a tax lien?

A tax lien is a special type of lien that is filed by the government against the assets of an individual or entity who fails to pay their taxes. Thus, if an individual or entity refuses to pay their taxes, then the government may impose a lien on their assets.

What happens if an entity refuses to pay taxes?

Thus, if an individual or entity refuses to pay their taxes, then the government may impose a lien on their assets. If an individual or entity refuses to pay their taxes even after a lien is in place, then the government can seize the assets that the lien is attached to.

Why can't I pay my taxes?

The amount was already paid off in full; The debtor is seeking an alternative collection method (e.g., installment agreement); The debtor is not able to pay their taxes because of a specific reason, such as having a terminal illness, not being employed, or only receiving income through welfare payments;

What happens if you have a federal tax lien on your home?

What if there is a federal tax lien on my home? If there is a federal tax lien on your home, you must satisfy the lien before you can sell or refinance your home. There are a number of options to satisfy the tax lien. Normally, if you have equity in your property, the tax lien is paid (in part or in whole depending on the equity) ...

When is a tax lien paid?

Normally, if you have equity in your property, the tax lien is paid (in part or in whole depending on the equity) out of the sales proceeds at the time of closing. If the home is being sold for less than the lien amount, the taxpayer can request the IRS discharge the lien to allow for the completion of the sale.

Can a tax lien be made secondary to a mortgage?

Taxpayers or lenders also can ask that a federal tax lien be made secondary to the lending institution's lien to allow for the refinancing or restructuring of a mortgage. The IRS currently is working to speed requests for discharge or mortgage restructing to assist taxpayers during this economic downturn. To assist struggling taxpayers, the IRS ...

What is a tax lien?

A levy takes your property or assets, where a lien secures the government’s interest in your property. A federal tax lien is a legal claim to your property (such as real property, securities and vehicles), including property that you acquire after the lien arises. If the IRS files a lien against your business, it attaches to all business property ...

What happens if you file a lien against your business?

If the IRS files a lien against your business, it attaches to all business property and to all rights to business property, including accounts receivable. A lien is just one of the collection procedures the IRS may use if you file or pay your taxes late. Publication 594, The IRS Collection Process, helps you understand the entire IRS collection ...

What to do if IRS is not responding?

If your IRS problem is causing you financial hardship, you’ve tried repeatedly and aren’t receiving a response from the IRS, or you feel your taxpayer rights aren’t being respected, consider contacting the Taxpayer Advocate Service (TAS).

How long does a lien stay on your credit report?

However, if the IRS releases a lien, it remains on your credit report for many years. A lien withdrawal, discussed below, however, removes the lien from your credit report.

What is a discharge on a lien?

Other situations with liens that might apply to you. A “discharge” removes the lien from specific property. For example, if you want to sell a certain piece of property that’s under a lien and intend to use part or all proceeds to pay your tax debt, you can apply for a Certificate of Discharge.

When is a lien filed in bankruptcy?

The lien was filed during a bankruptcy automatic stay period, when the IRS generally stops most collection activity, or. It’s in your best interest, as determined by the Taxpayer Advocate and in the best interest of the government. For example, this could include when your debt is satisfied and you request a withdrawal.

Can you ask IRS to withdraw a lien?

If you’ve paid your tax debt or fully paid your accepted Offer in Compromise and , if applicable, the outstanding amount of any related collateral agreement, and the lien was released, you can ask the IRS in writing to withdraw the lien. The IRS will generally do that, so long as:

How to avoid a tax lien?

Avoid a Lien. You can avoid a federal tax lien by simply filing and paying all your taxes in full and on time. If you can’t file or pay on time, don’t ignore the letters or correspondence you get from the IRS. If you can’t pay the full amount you owe, payment options are available to help you settle your tax debt over time.

How to withdraw a tax lien?

The other option may allow withdrawal of your Notice of Federal Tax Lien if you have entered in or converted your regular installment agreement to a Direct Debit installment agreement. General eligibility includes: 1 You are a qualifying taxpayer (i.e. individuals, businesses with income tax liability only, and out of business entities with any type of tax debt) 2 You owe $25,000 or less (If you owe more than $25,000, you may pay down the balance to $25,000 prior to requesting withdrawal of the Notice of Federal Tax Lien) 3 Your Direct Debit Installment Agreement must full pay the amount you owe within 60 months or before the Collection Statute expires, whichever is earlier 4 You are in full compliance with other filing and payment requirements 5 You have made three consecutive direct debit payments 6 You can’t have defaulted on your current, or any previous, Direct Debit Installment agreement.

What is a discharge from a lien?

A "discharge" removes the lien from specific property. There are several Internal Revenue Code (IRC) provisions that determine eligibility. For more information, refer to Publication 783, Instructions on How to Apply for Certificate of Discharge From Federal Tax Lien PDF and the video Selling or Refinancing when there is an IRS Lien.

What is a lien on a business?

Assets — A lien attaches to all of your assets (such as property, securities, vehicles) and to future assets acquired during the duration of the lien. Credit — Once the IRS files a Notice of Federal Tax Lien, it may limit your ability to get credit. Business — The lien attaches to all business property and to all rights to business property , ...

What happens to a business lien after bankruptcy?

Bankruptcy — If you file for bankruptcy, your tax debt, lien, and Notice of Federal Tax Lien may continue after the bankruptcy.

How long does it take to get rid of a tax lien?

Paying your tax debt - in full - is the best way to get rid of a federal tax lien. The IRS releases your lien within 30 days after you have paid your tax debt. When conditions are in the best interest of both the government and the taxpayer, other options for reducing the impact of a lien exist.

How much do you owe on a tax lien?

individuals, businesses with income tax liability only, and out of business entities with any type of tax debt) You owe $25,000 or less (If you owe more than $25,000, you may pay down the balance to $25,000 prior to requesting withdrawal of the Notice of Federal Tax Lien)

Understanding the Lien Process

A tax lien may exist against you after the IRS has assessed how much you owe in taxes, interest, and any fees, and provides you notice of this debt. If you fail or refuse to pay what the IRS requests, then a federal tax lien is executed.

How to Avoid or Remedy a Lien

Having a lien against you is one of the worst things that can happen to you from a financial standpoint. The best way to avoid a lien is simply to file your taxes accurately when required, and to pay all taxes owed.

How an Experienced Florida Tax & Lien Attorney Can Help

An attorney who is skilled in tax law can help you to understand the possible ramifications of a lien and how to mitigate the fallout, as well as repayment options. At the law offices of Ronald Cutler, P.A., we work for you. We pride ourselves on client satisfaction and personalized services, and will arrange our schedule to work with yours.

How long does it take to get a lien discharged?

It can take the IRS 45-60 days to approve the application, so prompt action is best to manage delays in your closing.

Can the IRS remove a lien on your home if you have no equity?

The IRS can agree to remove the tax lien even if you have no home equity and cannot pay at all. Here are two examples, one demonstrating the lien removal process if you have some leftover home equity, the other if you do not:

What does it mean when the IRS places a lien on your home?

What Does This Mean for You? When the IRS places a lien on your home, they are claiming a portion of that property value in lieu of the debt owed. A federal tax lien can negatively affect every aspect of your life, from your credit score to new property and selling your home.

How to avoid a lien on your house?

How to Prevent an IRS Lien on Your House. Responding to a letter or notice from the IRS can be daunting. It is important to remember that even when you owe a high amount, there are options to help you address your tax debt. Whatever you do, don’t avoid or ignore correspondence from the IRS, as it can grow into a much larger issue.

What happens when you have a federal lien on your property?

When a federal tax lien is applied to your property, a public Notice of Federal Tax Lien is published. You can request to have this notice withdrawn in two circumstances: You have paid your tax debt and it has been released. To qualify, you must have filed fully compliant tax returns for the past three years, including personal, business, ...

What is lien attached to new assets?

Attaches to New Assets. As long as you owe taxes to the IRS , the associated lien will carry over to all eligible property and any new property you acquire. This can include real estate, financial assets, and personal property such as vehicles and furniture. Until you have paid your debt in full or made acceptable payment arrangements, ...

What is a federal tax lien?

A federal tax lien is the federal government’s way of claiming unpaid taxes by laying claim to your property, in order to protect their financial interest. Prior to placing a lien, the IRS will send a Notice and Demand for Payment explaining the amount of tax owed. You are responsible for contacting the IRS to resolve your account, ...

What happens if you don't pay your taxes?

Failure to pay your taxes can have serious repercussions in both the short and long term. If you are a homeowner, the IRS may place a lien on your home for failure to pay your tax debt. A federal tax lien can cause numerous complications in your personal, financial, and business affairs, so it is important to understand what ...

How long does it take to get a lien off your house?

If you pay the debt in full, the IRS will release the lien within 30 days. This is the easiest and quickest way to remove the lien on your home. If you are unable to pay the full amount, there are other options available to limit the lien’s impact.

Popular Posts:

- 1. how to be a lawyer quick youtube

- 2. who is oj lawyer

- 3. lawyer continued collecting payment when case was over

- 4. how much does a good lawyer make

- 5. how to get free immigration lawyer in houston

- 6. how many cle creduts lawyer veorgua

- 7. why wasn't i allowed a lawyer for my traffic violation

- 8. how much will a pro lawyer cost

- 9. freddie highmore lived in what european city as a lawyer?

- 10. bald headed actor who plays a lawyer