To report payments to an attorney on Form 1099-MISC, you must obtain the attorney's TIN. You may use Form W-9, Request for Taxpayer Identification Number and Certification, to obtain the attorney's TIN. An attorney is required to promptly supply its TIN whether it is a corporation or other entity, but the attorney is not required to certify its TIN.

If the payment to that lawyer is $600 or more and made in connection with your trade or business, the payment must be reported in box 10 of IRS Form 1099-MISC. A settlement payment to the lawyer may also require an IRS Form 1099-MISC to report the payment to the claimant, even though the payment is made to the lawyer.Jan 14, 2021

Full

AnswerWhat 1099 is used for lawyers?

Of course, the basic Form 1099 reporting rule (for lawyers and everyone else) is that each person engaged in business and making a payment of $600 or more for services must report it on a Form 1099. The rule is cumulative, so while one payment of $500 wouldn’t trigger the rule, two payments of $500 to a single payee during the year require a Form 1099 for the full $1,000.

Which 1099 do attorneys get?

Currently, we still need the 1099-MISC form, a form which reports miscellaneous income such as payments to attorneys and rent ... pay $600 or more to them will need to use the form. Do tax forms get e a 1099-NEC? It normally serves independent contractors ...

Why do attorneys get 1099?

Lawyers receive and send more Forms 1099 than most people, in part because of tax laws that single them out. Lawyers, IRS Audits, and Forms 1099. Lawyers make good audit subjects because they often handle client funds, and many also tend to have high incomes. Since 1997, most payments to lawyers must be reported on a Form 1099.

When do attorneys get 1099s?

require a Form 1099 for the full $1,000. Lawyers must issue Forms 1099 to expert witnesses, jury consultants, investigators and even co-counsel where services are performed and the payment is $600 or more. A notable exception from the normal $600 rule is payments to corporations. Payments made to a corporation for services are generally exempt.

What do 1099 lawyers need to know?

Who must issue a 1099?

When do you send 1099 to IRS?

What is a 1099?

What is legal payment?

How to maximize your law firm's taxes?

How much does an insurance company pay to settle a claim?

See more

Do you send 1099 to lawyers?

The 1099-NEC reporting requirements only apply to businesses or organizations, and only in specific conditions. A business has to provide an attorney or law firm a 1099 if the business pays that attorney more than $600 for legal services in the same calendar year.

Do attorneys always receive 1099?

A client who pay fees to a law firm in excess of $600 in the course of the client's trade or business is required to issue a Form 1099. In the past, however, if the law firm was a corporation then no Form 1099 was required. As of January 1, 1998 a Form 1099 will be required even though the firm is a corporation.

What 1099 form do I use for lawyers?

1099-NECWhen to report attorney payments on a 1099-NEC. Rule of thumb: Report payments to an attorney on Form 1099-NEC if you were their client. Of course, the reporting requirements we went through above still apply: The payments need to be $600 or more and rendered for work-related services.

Does an attorney get a 1099-NEC or 1099-Misc?

Attorneys' fees of $600 or more paid in the course of your trade or business are reportable in box 1 of Form 1099-NEC, under section 6041A(a)(1).

Do payments to attorneys do 1099-MISC?

If the payment to that lawyer is $600 or more and made in connection with your trade or business, the payment must be reported in box 10 of IRS Form 1099-MISC. A settlement payment to the lawyer may also require an IRS Form 1099-MISC to report the payment to the claimant, even though the payment is made to the lawyer.

Do you issue 1099 for professional services?

Payments made to vendors/independent contractors of $600 or more for services such as legal and professional fees, advertising, maintenance, repairs, commissions, etc. must be reported on the new Form 1099-NEC. This includes payments made to individuals, partnerships or LLCs and, in some cases, even corporations.

Do I need to send a 1099 to my accountant?

If Your Accounting Firm is Organized as a Partnership, the IRS Requires 1099s for Fees Paid. The IRS requires businesses, self-employed individuals, and not-for-profit organizations to issue Form 1099-MISC for professional service fees of $600 or more paid to accountants who are not corporations.

What payments are excluded from a 1099-NEC and 1099-MISC?

Which payments are excluded from the 1099-MISC and 1099-NEC form? Payments to 1099 vendors made via credit card, debit card, or third party system, such as PayPal, are excluded from the 1099-MISC and 1099-NEC calculations. This is because the financial institution reports these payments, so you don't have to.

What does gross proceeds paid to an attorney mean?

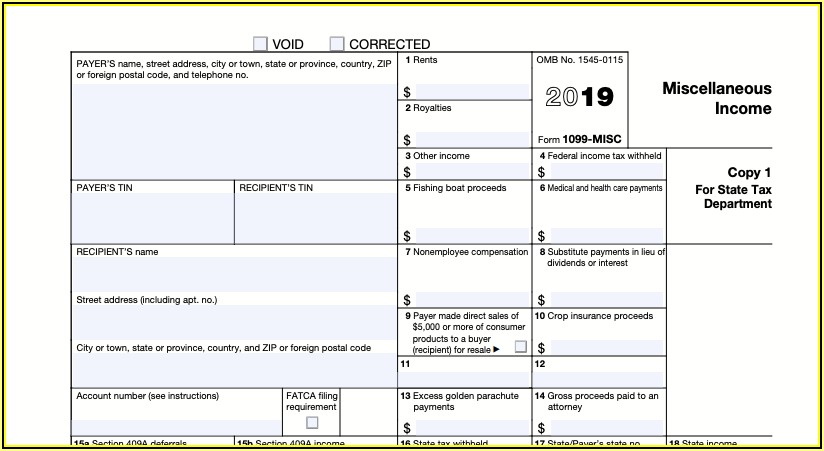

Gross proceeds are payments that: Are made to an attorney in the course of your trade or business in connection with legal services, but not for the attorney's services, for example, as in a settlement agreement; Total $600 or more; and. Are not reportable by you in box 7.

What box do legal fees go in on 1099?

Attorney fees paid in the course of your trade or business for services an attorney renders to you are reported in box 1 of Form 1099-NEC. Gross proceeds paid to an attorney in connection with legal services, but not for the attorney's services, are reported in box 10 of Form 1099-MISC.

What is difference between 1099-MISC and 1099-NEC?

The 1099-NEC is now used to report independent contractor income. But the 1099-MISC form is still around, it's just used to report miscellaneous income such as rent or payments to an attorney. Although the 1099-MISC is still in use, contractor payments made in 2020 and beyond will be reported on the form 1099-NEC.

What happens if I use 1099-MISC instead of 1099-NEC?

If I received a 1099-misc instead of a 1099-nec, does that have to be corrected? No difference if you enter the 1099NEC or just enter it all as Cash or General. Only the total of 1099NEC & cash goes to Schedule C line 1. Doesn't matter how you enter it as long as the total is the same or more than the 1099NECs you got.

1099 Reporting Requirements For 2021-2022 Tax Season

1099 Reporting Requirements For 2021-2022 Tax Season. Here is everything you need to know about the 1099 reporting requirements. Learn more.

IRS 1099 Reporting Requirements for Attorneys - OSB PLF

www.osbplf.org April 2017 Malpratie Preention Eduation for regon Layers DISCLAIMER This material is provided for informational purposes only and does not establish, report, or create the standard of care for attorneys in Oregon, nor does it represent a complete analysis of the topics presented.

IRS Form 1099 Rules for Settlements and Legal Fees

IRS Forms 1099 match income and Social Security numbers. Lawyers receive and send more Forms 1099 than most people, in part due to tax laws that single them out. The tax code requires companies making payments to attorneys to report the payments to the IRS on a Form 1099.

When to Issue a 1099: Everything You Need to Know

When to Issue a 1099. A 1099 form is used to document wages paid to a freelance worker or independent contractor.While many business owners aren't sure when to issue a 1099 form to an independent contractor, doing so is an important part of tax compliance.

How to report a 1099 to an attorney?

To report payments to an attorney on Form 1099-MISC, you must obtain the attorney's TIN. You may use Form W-9, Request for Taxpayer Identification Number and Certification, to obtain the attorney's TIN. An attorney is required to promptly supply its TIN whether it is a corporation or other entity, but the attorney is not required to certify its TIN. If the attorney fails to provide its TIN, the attorney may be subject to a penalty under section 6723 and its regulations, and you must backup withhold on the reportable payments.

What is attorney fee on 1099?

The term "attorney" includes a law firm or other provider of legal services. Attorneys' fees of $600 or more paid in the course of your trade or business are reportable in box 1 of Form 1099-NEC, under section 6041A(a)(1). Gross proceeds paid to attorneys. Under section 6045(f), report in box 10 payments that:

When is the 1099-NEC due?

114-113, Div. Q, sec. 201, accelerated the due date for filing Form 1099 that includes nonemployee compensation (NEC) from February 28 to January 31 and eliminated the automatic 30-day extension for forms that include NEC. Beginning with tax year 2020, use Form 1099-NEC to report nonemployee compensation.

How much do you report royalty payments on a 1099?

Enter gross royalty payments (or similar amounts) of $10 or more. Report royalties from oil, gas, or other mineral properties before reduction for severance and other taxes that may have been withheld and paid. Do not include surface royalties. They should be reported in box 1. Do not report oil or gas payments for a working interest in box 2; report payments for working interests in box 1 of Form 1099-NEC. Do not report timber royalties made under a pay-as-cut contract; report these timber royalties on Form 1099-S, Proceeds From Real Estate Transactions.

What to report on W-2 after death?

When an employee dies during the year, you must report the accrued wages, vacation pay, and other compensation paid after the date of death. If you made the payment in the same year the employee died, you must withhold social security and Medicare taxes on the payment and report them only as social security and Medicare wages on the employee's Form W-2 to ensure that proper social security and Medicare credit is received. On the Form W-2, show the payment as social security wages (box 3) and Medicare wages and tips (box 5) and the social security and Medicare taxes withheld in boxes 4 and 6; do not show the payment in box 1 of Form W-2.

Do you report attorney fees on 1099?

Are not reportable by you in box 1 of Form 1099-NEC. Generally, you are not required to report the claimant's attorney's fees. For example, an insurance company pays a claimant's attorney $100,000 to settle a claim. The insurance company reports the payment as gross proceeds of $100,000 in box 10.

Do you have to report a hospital payment?

However, you are not required to report payments made to a tax-exempt hospital or extended care facility or to a hospital or extended care facility owned and operated by the United States (or its possessions), a state, the District of Columbia, or any of their political subdivisions, agencies, or instrumentalities.

Why do lawyers send 1099s?

Copies go to state tax authorities, which are useful in collecting state tax revenues. Lawyers receive and send more Forms 1099 than most people, in part due to tax laws that single them out. Lawyers make good audit subjects because they often handle client funds. They also tend to have significant income.

When do you get a 1099 from a law firm?

Forms 1099 are generally issued in January of the year after payment. In general, they must be dispatched to the taxpayer and IRS by the last day of January.

What if the lawyer is beyond merely receiving the money and dividing the lawyer’s and client’s shares?

What if the lawyer is beyond merely receiving the money and dividing the lawyer’s and client’s shares? Under IRS regulations, if lawyers take on too big a role and exercise management and oversight of client monies, they become “payors” and as such are required to issue Forms 1099 when they disburse funds.

What is the exception to the IRS 1099 rule?

Payments made to a corporation for services are generally exempt; however, an exception applies to payments for legal services. Put another way, the rule that payments to lawyers must be the subject of a Form 1099 trumps the rule that payments to corporation need not be. Thus, any payment for services of $600 or more to a lawyer or law firm must be the subject of a Form 1099, and it does not matter if the law firm is a corporation, LLC, LLP, or general partnership, nor does it matter how large or small the law firm may be. A lawyer or law firm paying fees to co-counsel or a referral fee to a lawyer must issue a Form 1099 regardless of how the lawyer or law firm is organized. Plus, any client paying a law firm more than $600 in a year as part of the client’s business must issue a Form 1099. Forms 1099 are generally issued in January of the year after payment. In general, they must be dispatched to the taxpayer and IRS by the last day of January.

How does Larry Lawyer earn a contingent fee?

Example 1: Larry Lawyer earns a contingent fee by helping Cathy Client sue her bank. The settlement check is payable jointly to Larry and Cathy. If the bank doesn’t know the Larry/Cathy split, it must issue two Forms 1099 to both Larry and Cathy, each for the full amount. When Larry cuts Cathy a check for her share, he need not issue a form.

What percentage of 1099 does Larry get?

The bank will issue Larry a Form 1099 for his 40 percent. It will issue Cathy a Form 1099 for 100 percent, including the payment to Larry, even though the bank paid Larry directly. Cathy must find a way to deduct the legal fee.

How much is the penalty for not filing 1099?

Most penalties for nonintentional failures to file are modest—as small as $270 per form . This penalty for failure to file Forms 1099 is aimed primarily at large-scale failures, such as where a bank fails to issue thousands of the forms to account holders; however, law firms should be careful about these rules, too.

What is the most common 1099?

But let’s look at the realities and the different boxes on a Form 1099 before you decide. The most common version used is Form 1099-MISC, for miscellaneous income. But to discuss it, we also must also talk about the newest one, Form 1099-NEC. Up until 2020, if you were paying an independent contractor, you reported it on Form 1099-MISC, in box 7, for non-employee compensation.

When do you send a 1099?

Some businesses and law firms prefer to issue Forms 1099 at the time they issue checks, rather than in January of the following year. For example, if you are mailing out thousands of checks to class action recipients, you might prefer sending a single envelope that includes both check and Form 1099, rather than sending a check and later doing another mailing with a Form 1099.

Why is gross proceeds paid to an attorney important?

Why is the gross proceeds paid to an attorney category so important? For one thing, gross proceeds reporting for lawyers is not counted as income to the lawyer. Any payment to a lawyer is supposed to be reported, even if it’s entirely the client’s money to close a real estate deal. Case settlement proceeds count as gross proceeds, too.

What box is gross proceeds paid to an attorney?

Gross proceeds paid to an attorney for 2019 and prior years was box 14. But now, it is reported in box 10 of the new 2020 Form 1099-MISC. This box is only for reporting payments to lawyers. It turns out that there are numerous special Form 1099 rules for lawyers.

What box is 1099-MISC?

For 2020 and subsequent-year payments, your choices on Form 1099-MISC are more limited. Most payments are recorded in box 3, as other income. For lawyers settling cases, though, “gross proceeds paid to an attorney” is the most important category. Many lawyers may not see Form 1099 that arrive at their office, but they should be aware of this important box on the form, and what it means for their taxes.

When will 1099-MISC be reported?

It impacts their clients too. Up through 2019 payments, IRS Form 1099-MISC box 14 was for gross proceeds paid to an attorney. That means the payments you received in 2019 that were reported in early 2020 were on these 2019 forms. For payments in 2020, they will be reported in January of 2021 on a new version of Form 2020-MISC.

What is a 1099 NEC?

In other words, Form 1099-NEC reports a payment for services. For 2019 and prior years, putting income in box 7 of a Form 1099-MISC usually tipped the IRS off that this person should not only be paying income tax but also paying self-employment tax.

Who is required to issue a 1099?

For taxable settlements, the defendant is required to issue a 1099 to the plaintiff under § 6041. In addition, if the proceeds are jointly payable to attorney and plaintiff, the defendant is required to issue a 1099 to attorney under § 6045 as amounts paid “in connection with legal services.”.

What is the IRS 1099?

Generally speaking, information returns like Form 1099-MISC (“1099”) are necessary for payments of $600.00 or more distributed in the course of business.

Can an attorney receive a separate check for damages?

To avoid a situation whereby the IRS interprets the entire settlement as income to the attorney, the attorney can simply request a separate check payable to plaintiff for damages and one payable to attorney for attorney’s fees and reimbursable costs: only the amounts paid to attorney are reportable under § 6045.

Do you have to issue a 1099 for a settlement?

Consequently, defendants issuing a settlement payment, or insurance companies issuing a settlement payment on behalf of the defendant, are required to issue a 1099 to the plaintiff unless the settlement qualifies for one of the tax exceptions. See IRC § 6041 . In some cases, a tax provision in the settlement agreement characterizing the payments can result in their exclusion from income. Although tax provisions are not controlling, the IRS is generally reluctant to override the intent of the parties. Accordingly, any settlement payments made expressly for nontaxable damages are excluded from the 1099 reporting requirements.

What is a 1099-MISC?

This is a form that means "miscellaneous income". You'll send it out to any independent contractors who did business with you in the last year. It is the equivalent of a W-2 form for outsourced work. You've got until January 31st to get these forms in order and sent out. Not meeting this deadline will cost anywhere from $30-100 a form.

What is a W-2 form?

You'll send it out to any independent contractors who did business with you in the last year. It is the equivalent of a W-2 form for outsourced work. You've got until January 31st to get these forms in order and sent out.

Who does a 1099 need to be sent to?

Form 1099s must be sent to sole proprietors, S corporations, LLCs and partnerships. As a general rule, a business doesn't need to issue a 1099 to a corporation or an LLC organized as a corporation. There are a few exceptions to that rule, however.

What is a 1099-MISC?

The 1099 reports the name, address and identification number of the recipient. It also details the amount of payments made to him during the tax year and the nature of the income.

What box do you report attorney fees paid in?

Report any attorney fees paid in box 7, regardless of whether or not you were the recipient of the legal services. If you paid anything else to the attorney that doesn't qualify as legal fees, report that in box 14. For example, an insurance company that settles a claim would report the settlement proceeds in box 14.

Do businesses have to send 1099s?

This means that businesses are always responsible for sending 1099s but individuals don't always have to. For example, if you're a landlord and you paid legal fees to recover payment from a tenant, you're responsible for sending a 1099-MISC.

Do attorneys have to report fees on 1099?

However, any attorney fees paid should be reported on a 1099 regardless of the law firm's business structure , assuming the fees totaled more $600 during the year and they were incurred in the course of a taxpayer's trade or business.

Who needs a 1099?

A 1099 is required for any worker who is not a U.S. citizen. It is the onus of the business owner to determine whether a contractor or vendor is a citizen. You can ask them to fill out Form W-8BEN for this purpose.

Who Requires a Form 1099?

This form needs to be sent to subcontractors and vendors to whom you paid more than $600 in a calendar year, including all estates, individuals, limited partnerships, or limited liability companies?

When are 1099s due?

Taxpayers must mail Form 1099 to vendors by Jan. 31. The transmittal form is due to the IRS by Feb. 28. If you have an accountant, he or she can submit these forms electronically by March 31.

What is a 1099 form?

A 1099 form is used to document wages paid to a freelance worker or independent contractor. While many business owners aren't sure when to issue a 1099 form to an independent contractor, doing so is an important part of tax compliance. Here's what you need to know about this important documentation for freelance workers.

What percentage of your pay can you withhold if you don't fill out a W-9?

If they have not filled out a W-9 or if the information is missing, you are allowed to withhold 28 percent of their pay and send it to the IRS. 2. Gather 1099s. You have to use specific forms picked up from the post office or IRS center; downloaded and printed versions are not allowed.

How much is the penalty for not submitting 1099?

Penalties for not providing a required 1099-MISC form range from $30 to $100 depending on when you finally issue the form. The cap on this penalty is $1.5 million annually per business. In addition, businesses who refuse this requirement are charged a minimum fee of $250 per form.

When is the 1099 deadline?

Jan. 31 is a new deadline, so don't get it confused with the previous end-of-February deadline. Also, check with your state to determine whether you need to file a 1099-MISC form. If you miss the deadline, talk with your accountant.

What do 1099 lawyers need to know?

What A 1099 Lawyer Needs to Know When Filing Taxes. According to the American Bar Association, in 2019, over 1.3 million attorneys actively practiced in the United States, with approximately 63 percent practicing in a solo 1099 lawyer or small firms (2-9 attorneys). However, no matter if a lawyer practices in a larger firm or hung out her own ...

Who must issue a 1099?

A lawyer or law firm paying fees to co-counsel (or referral fee) to a lawyer must issue a Form 1099.

When do you send 1099 to IRS?

Form 1099s are based on income received during the calendar year, with the reporting entity generally the due date for sending a copy of the 1099 to the recipient of the payments by January 31st of the following year and a copy to the IRS by the last day in February or March 31st if electronic filing, also in the following year. However, with the 1099-NEC, as discussed further below, you must send a copy to recipients and to the IRS by the same date – January 31st.

What is a 1099?

As a review, Form 1099 is an informational return, typically reporting certain types of income. Currently, over 20 different types of Form 1099 exist, including 1099-MISC (for miscellaneous income such as that earned by self-employed individuals), 1099-INT (for interest income, such as that received from a savings bank account), and 1099-DIV (for dividend payments received from investments).

What is legal payment?

Legal types of payments are made to an attorney or law firm in the course of the business or trade, excluding personal services provided by an attorney. Examples of these payments include those related to a settlement agreement with another person or business;

How to maximize your law firm's taxes?

By strategically planning your law firm's taxes, you can maximize your deductions by keeping careful paperwork and records of your business expenses throughout the year.

How much does an insurance company pay to settle a claim?

An insurance company pays a claimant's attorney $100,000 to settle a claim. The insurance company reports the payment as gross proceeds of $100,000 in box 10. However, the insurance company does not have a reporting requirement for the claimant's attorney's fees subsequently paid from these funds in the full amount.

Reporting Requirements

The IRS requires taxpayers to file an information return in connection with certain transactions and may assess penalties for failure to comply with the rules. Generally speaking, information returns like Form 1099-MISC (“1099”) are necessary for payments of $600.00 or more distributed in the course of business…

Taxable v. Nontaxable

- So what settlement proceeds are taxable? All amounts from any source are included in gross income unless a specific exception exists. For damages, the two most common exceptions are amounts paid for certain discrimination claims and amounts paid “on account of” physical injury. This covers observable bodily harm and may include emotional distress if there is a causal link t…

Attorney Or Client?

- For taxable settlements, the defendant is required to issue a 1099 to the plaintiff under § 6041. In addition, if the proceeds are jointly payable to attorney and plaintiff, the defendant is required to issue a 1099 to attorney under § 6045 as amounts paid “in connection with legal services.” As a result, both attorney and plaintiff receive 1099s f...

Recommendation

- All taxpayers need to issue 1099s for payments to attorneys, including payments from attorneys to other attorneys, as well as for payments under the $600.00 rule. In litigation, this is the responsibility of the defendant or the defendant’s insurance company. One way to avoid the necessity of requesting separate checks from the defendant or the defendant’s insurance comp…

Popular Posts:

- 1. the town who had a poor lawyer another layer moved to town

- 2. sc law how to get my husbands bank account without lawyer

- 3. what is immigration lawyer ?

- 4. what does a lawyer assistant do

- 5. lawyer who defended ray lewis

- 6. factors to consider when hiring a traumatic brain injury lawyer

- 7. what you need to be a cps defense lawyer

- 8. what kind of special educations should a state tax lawyer have

- 9. who was bill clinton's lawyer in the paula jones case

- 10. what is a fair lawyer